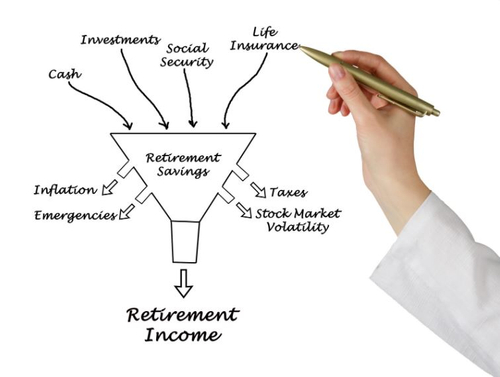

Retirement is a major milestone that brings many life changes. One thing that doesn't change for most people: the fear of running out of money. In fact, one of the most frequently reported retirement worries is outliving savings and investments. And interestingly, this is a concern across all ages – many don’t think they’ve built a nest egg large enough to last through retirement. Now is the time to face your fears. Yes, there are a lot of ways you could go broke in retirement, but many can be averted with careful planning. Here are seven ways you could run out of money in retirement – and ways to avoid them.

You could go broke in retirement if: