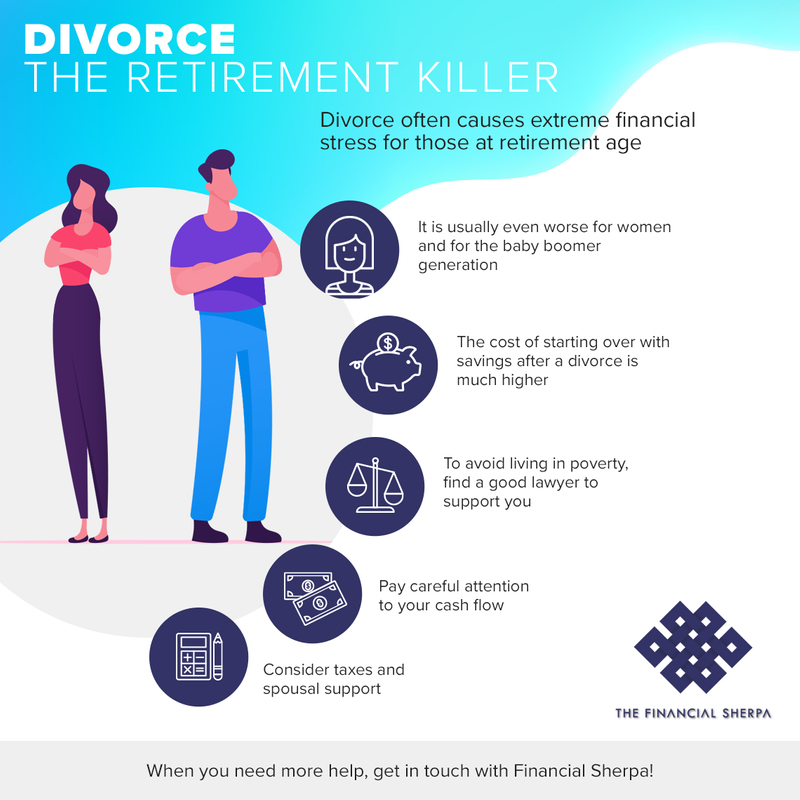

Now, while every divorce is unique in its own way, the reality is that there is usually one common theme in all divorces – it destroys retirement. And while every divorced person feels the financial impact, baby boomers suffer more – and the impact among women baby boomers is among the worse.

According to a study from economists Claudia Olivetti of Boston College and Dana Rotz of Mathematica Policy Research, the later in life a woman divorces, the more likely she will be working full time late in life.

Analyzing data from over 50,000 women, the researchers found that women who divorced in their 50s were more than 10 percentage points more likely to be working full time from ages 50 to 74 – compared to women who divorced before age 30.

And the immediate financial impact of divorce goes beyond legal fees. While the best scenarios might see a 50/50 split of assets, the pie is always smaller than both parties realize. And once assets are divided, say in half, then the expenses double – two homes to manage or rents to cover, two utility bills to pay, two car payments to make, etc.

Why is it worse for women, generally speaking? For many women – especially those with children – I often see them trade away retirement assets to hold onto the family home. And sadly, this means they need to start saving for retirement all over again – without the benefit of time.